06 October, 2012

02 October, 2012

24 September, 2012

Update 9/24

The previously suggested strategy to buy dips in the market seems to hold well. I have been succesful trading .5% swings. It seems like the market sentiment is a bit too positive at the moment for the market to make another sustained up move just yet. We probably need to see a bit of a flushout beyond these sideways consolidation movements as well as a new trigger, like q3 earnings. Sell rallies and buy the 2% dip.

22 September, 2012

Companies continue to lower Q3 guidance

This is in line with my yearly forecast point and an important trading aspect to take in to account, basically, on index level, there is no growth. At best there is 0-5% growth even next year. That said, there is not a great danger to a traditional cyclical business downturn either. So what we have is this low growth, new normal, whatever, stuff going on for some time to come.

This implies an investor need to pay attention to

a) sentiment swings.

b) p/e-levels (base case interval 11-15).

c) central banks, the monetary base and price equities in terms of gold, oil etc.

So far, 103 companies in the index have provided guidance for the third quarter. Of those, 80% have guided below Wall Street consensus estimates, according to John Butters, senior earnings analyst at FactSet. That’s the most negative outlook since FactSet began tracking the figures in the first quarter of 2006.

Adding insult to injury, S&P 500 companies are projected to see earnings drop year-over-year for the first time in 12 quarters. Third-quarter earnings are currently estimated to drop by 2.7% for the S&P 500 as a whole, the worst forecast growth rate over the past 12 quarters, Butters added. At the beginning of the quarter, analysts had been forecasting earnings growth of 1.9%.

http://blogs.marketwatch.com/thetell/2012/09/21/many-sp-500-companies-forecasting-third-quarter-misses/

In another recent article, this phenomena is demonstrated by a simple dividend model.

The model, at least the variant I will focus on for this column, is breathtakingly simple. It says that the market’s long-term return will be a function of just two things: the current dividend yield and real growth in earnings and dividends.

Since this latter growth rate over the last century has averaged about 1.4%, we can forecast what the market will do over the next decade by simply adding the market’s current dividend yield, the assumed real growth rate of 1.4%, and expected inflation.

These three components today add up to a nominal return of 5.6% annualized, according to Rob Arnott, founder of Research Affiliates, an investment advisory firm — or 3.4% in real terms.

http://www.marketwatch.com/story/stocks-future-return-just-56-annualized-2012-09-21

This implies an investor need to pay attention to

a) sentiment swings.

b) p/e-levels (base case interval 11-15).

c) central banks, the monetary base and price equities in terms of gold, oil etc.

So far, 103 companies in the index have provided guidance for the third quarter. Of those, 80% have guided below Wall Street consensus estimates, according to John Butters, senior earnings analyst at FactSet. That’s the most negative outlook since FactSet began tracking the figures in the first quarter of 2006.

Adding insult to injury, S&P 500 companies are projected to see earnings drop year-over-year for the first time in 12 quarters. Third-quarter earnings are currently estimated to drop by 2.7% for the S&P 500 as a whole, the worst forecast growth rate over the past 12 quarters, Butters added. At the beginning of the quarter, analysts had been forecasting earnings growth of 1.9%.

http://blogs.marketwatch.com/thetell/2012/09/21/many-sp-500-companies-forecasting-third-quarter-misses/

In another recent article, this phenomena is demonstrated by a simple dividend model.

The model, at least the variant I will focus on for this column, is breathtakingly simple. It says that the market’s long-term return will be a function of just two things: the current dividend yield and real growth in earnings and dividends.

Since this latter growth rate over the last century has averaged about 1.4%, we can forecast what the market will do over the next decade by simply adding the market’s current dividend yield, the assumed real growth rate of 1.4%, and expected inflation.

These three components today add up to a nominal return of 5.6% annualized, according to Rob Arnott, founder of Research Affiliates, an investment advisory firm — or 3.4% in real terms.

http://www.marketwatch.com/story/stocks-future-return-just-56-annualized-2012-09-21

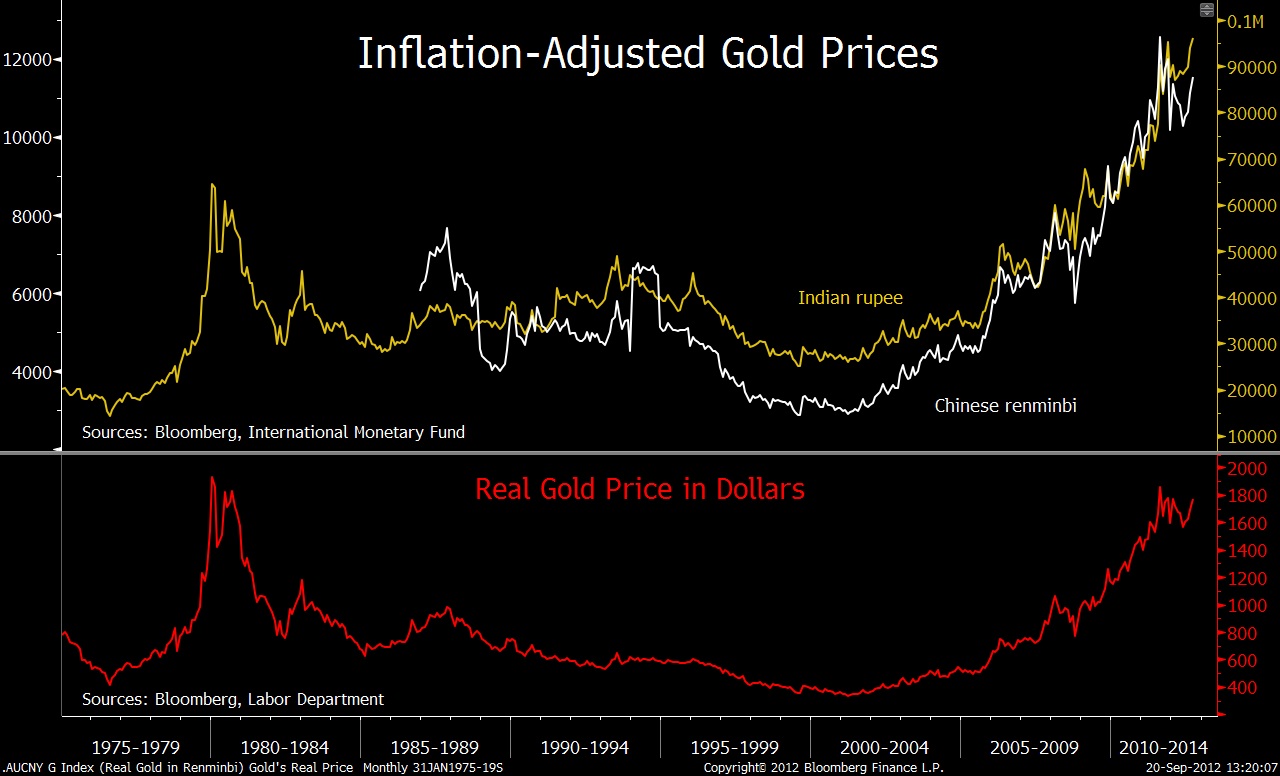

S&P 500 priced in gold and oil.

Is the stock market going up? Or is it just other things than the consumer price index getting more expensive?

Short SPX, Long Gold, one of my major trades for 2012 now that the next leg in central bank activism has been initiated and equities generally have squeezed away most of the risk premia.

Short SPX, Long Gold, one of my major trades for 2012 now that the next leg in central bank activism has been initiated and equities generally have squeezed away most of the risk premia.

|

| Short SPX, Long Gold. |

.png) |

| Short SPX, Long WTI

Ritholtz posted a relating chart with gold compared to the consumer price index. That is a flawed measure in my opinion since the consumer price index will never reflect inflation at this stage in the printing cycle.

|

Language transition of the blog

In hopes to generate more interest and feedback, the blog is now continuing its posting in english.

The blogs focus has long been centered mainly on major equity market developlements, central bank policy, housing markets and investment banking in general.

The writer is a long time investment banking operative in the nordic markets.

The blog is usually updated once a week but I will also add some old posts from 2008-2011 with material that has been especially appreciated by readers.

The blogs focus has long been centered mainly on major equity market developlements, central bank policy, housing markets and investment banking in general.

The writer is a long time investment banking operative in the nordic markets.

The blog is usually updated once a week but I will also add some old posts from 2008-2011 with material that has been especially appreciated by readers.

14 September, 2012

Update 9/14

Like the blog stated 3 days ago, central banks control the world. Open ended QE until unemployment is down to much lower levels, or something else happens before that, that is what we have before us. I would call it a world war in monetary policy. It's all in now and it is just to go with the flow. Asset classes will rise until the following scenario plays out: Food prices and other input prices rise to the point that these factors offset the positive wealth effect. At this turning point, reducing demand in the economy due to the high raw material / input prices and at the same time squeezing margins of companies. It is the only scenario that can derail this and it is not so different this time, actually it is pretty text book stuff. It is thus relative hyperinflation, perhaps not by historical standards but hyperinflation in the definition of further stimulus is no longer possible because it weakens rather than strengthens the economy. Another scenario is more political and is linked to how other countries react to the weakening of the dollar policy. The big movement is in the near future, however, completed and I will invest in buying 1-2% dips in the index next week.

11 September, 2012

Update 9/11

It has been some time since the last update. It was also a long time since I saw the market as boring as I do today. "Boring" needs to be interpreted in the right way though. It is important to understand that we live in a time with so-called "financial repression". Central banks have gone all in, and thereby controls currently the world's markets. Therefore we have a low volatility environment right now and will probably have it until something goes wrong, which would be a country within the EU get enough of cutbacks, leaving the euro, or central bank activity reaches end of the road, creating inflation and / or rising input prices and falling margins and / or final demand. It's not something I see happening in the next few months and will apply the strategy layed out below until further notice. Otherwise, there is little immediate threat to the economy other than the long-factors that have been in force for many years and treated in many previous posts. These fill but more the function of a cap on growth in general, and for workers in the western world in particular, and are not so much a significant negative for the stock market.

In this environment, daytrading probably needs to be limited compared to previous years. For myself, that means significant reaollocation aprox once a week. A more basic investor should apply a strong focus on minimizing costs and to switch focus to dividends.

Sentiment studies and anecdotal reports suggest a very, if not bearishly positioned, at least "not very long" investors. Although downside ahead will be limited as long central bank puts are in place, the upside will be limited by all the aforementioned factors raised on the blog many times and remain relevant. To make clear how extreme I look at central situation. I think next year the S & P 500 moves within a 10-15% range. Approximately 5% upside and 10% downside. I will act accordingly and work with mean reversion trading.

Directionally (weekly focus), my next activity will be in coming weeks to use dips of 1-2% in major indexes to swing trade the next leg up.

Mean reversion/Consolidition (daily focus), until that leg starts we will probably be stuck in this 1-2% or less consolidition phase.

Hedged bets (monthly foxus), will consist of

a) long short trade in precious metals vs industrial metals.

Some oil will be used for long trading as well but only on unrational SPR- or other rumour related dips.

b) long short trade within tech space, long tech companies with a brand/margins, short tech companies without a brand/margins (to really simplify the strategy, but really, that is it's core).

c) long worlds largest global companies, short more regional ones of same operational focus but limited to (most interesting) Europe.

As a general note on shorting I find it more and more difficult to identify good short sales. There are some in the tech space still though but many, like AMD, LXK, LOGI have already been slaughtered and should await squeezes until new shorts on these or long/short.

In this environment, daytrading probably needs to be limited compared to previous years. For myself, that means significant reaollocation aprox once a week. A more basic investor should apply a strong focus on minimizing costs and to switch focus to dividends.

Sentiment studies and anecdotal reports suggest a very, if not bearishly positioned, at least "not very long" investors. Although downside ahead will be limited as long central bank puts are in place, the upside will be limited by all the aforementioned factors raised on the blog many times and remain relevant. To make clear how extreme I look at central situation. I think next year the S & P 500 moves within a 10-15% range. Approximately 5% upside and 10% downside. I will act accordingly and work with mean reversion trading.

Directionally (weekly focus), my next activity will be in coming weeks to use dips of 1-2% in major indexes to swing trade the next leg up.

Mean reversion/Consolidition (daily focus), until that leg starts we will probably be stuck in this 1-2% or less consolidition phase.

Hedged bets (monthly foxus), will consist of

a) long short trade in precious metals vs industrial metals.

Some oil will be used for long trading as well but only on unrational SPR- or other rumour related dips.

b) long short trade within tech space, long tech companies with a brand/margins, short tech companies without a brand/margins (to really simplify the strategy, but really, that is it's core).

c) long worlds largest global companies, short more regional ones of same operational focus but limited to (most interesting) Europe.

As a general note on shorting I find it more and more difficult to identify good short sales. There are some in the tech space still though but many, like AMD, LXK, LOGI have already been slaughtered and should await squeezes until new shorts on these or long/short.

26 January, 2011

Forecast 2011

There has been long times between posts recently, which might be explained by the lower volatility in the markets. Previous posts have simply largely remained in force. Shorting the market has been devastating. I hedged myself by arguing for long commodities and short equities. It has worked out whether one have chosen pure commodity exposure or in the form of shares. Lately,

Before going outright long I will await a larger dip (5-10%). A simple trend line analysis shows that OMXS 30 is trending 40% annualized. Such a rise rate simply can not continue after the initial phase of the recovery and also completed fiscal stimulus / discounted. Now we are also facening budget constraints virtually all over the entire Western world, as well as policy changes in the China locomotive, where a clear shift towards domestic consumption to take place, which would go against earlier policy and be a disadvantage to most western export companies.

But a balanced view is needed on equities. Valuations measures (not adjusted cycle) and continued low interest rates, QE and allocation from bonds to stock market provides support for the markets.

Maybe the 70's scenario should continue to be the main business case, where we move sideways for a decade. Not quite as big rise and fall as during 2000-2010. Budgetary restrictions will be with us for over a decade years. The rebalance of wages all over the world, where emerging market wages increase and western market wages decrease/unemployment increases and government deficits increase as populations demand same service as previous generation. This is highly inflationary in a bad inflation way. Mostly the cost of needs will increase (i.e. energy, food etc). But this is merely a rebalancing of growth from western world to the eastern world. For global companies, this should not be limiting their growth, rather keeping their margins on a sustained high level (this time is different) since there cannot be wage increases in the western world. In addition to this major shift of the global work force, retirement schemes and non-favorable demographics as just adding extra on top of the problems of the west.

When it comes to the S&P 500, one needs to figure out what is a reasonable P/E during these times. Cyclically adjusted P/E's look very expensive and an average of individual years is flawed to look at as well due to the .com bubble. With the S&P near 1300 and profits, at best, around $ 93 for 2011 a P/E of 14 then gives 1302. P/E 14 does feel a bit on the high side in a scenario where GDP is growing below potential, interest rates are rising, dividends are below historical average, margins are historically high, and fiscal cutbacks kicks in, it feels high to me. But then margins are historically high and maybe not mean reverting any longer because of the structural change described above. Maybe one should view a range of P/E 11-15 as a reasonable measure and trade mean reverting around those levels in a period of very low general growth as well as central bank puts which both caps upside and downside.

Before going outright long I will await a larger dip (5-10%). A simple trend line analysis shows that OMXS 30 is trending 40% annualized. Such a rise rate simply can not continue after the initial phase of the recovery and also completed fiscal stimulus / discounted. Now we are also facening budget constraints virtually all over the entire Western world, as well as policy changes in the China locomotive, where a clear shift towards domestic consumption to take place, which would go against earlier policy and be a disadvantage to most western export companies.

But a balanced view is needed on equities. Valuations measures (not adjusted cycle) and continued low interest rates, QE and allocation from bonds to stock market provides support for the markets.

Maybe the 70's scenario should continue to be the main business case, where we move sideways for a decade. Not quite as big rise and fall as during 2000-2010. Budgetary restrictions will be with us for over a decade years. The rebalance of wages all over the world, where emerging market wages increase and western market wages decrease/unemployment increases and government deficits increase as populations demand same service as previous generation. This is highly inflationary in a bad inflation way. Mostly the cost of needs will increase (i.e. energy, food etc). But this is merely a rebalancing of growth from western world to the eastern world. For global companies, this should not be limiting their growth, rather keeping their margins on a sustained high level (this time is different) since there cannot be wage increases in the western world. In addition to this major shift of the global work force, retirement schemes and non-favorable demographics as just adding extra on top of the problems of the west.

When it comes to the S&P 500, one needs to figure out what is a reasonable P/E during these times. Cyclically adjusted P/E's look very expensive and an average of individual years is flawed to look at as well due to the .com bubble. With the S&P near 1300 and profits, at best, around $ 93 for 2011 a P/E of 14 then gives 1302. P/E 14 does feel a bit on the high side in a scenario where GDP is growing below potential, interest rates are rising, dividends are below historical average, margins are historically high, and fiscal cutbacks kicks in, it feels high to me. But then margins are historically high and maybe not mean reverting any longer because of the structural change described above. Maybe one should view a range of P/E 11-15 as a reasonable measure and trade mean reverting around those levels in a period of very low general growth as well as central bank puts which both caps upside and downside.

20 May, 2008

Leading indicators?

Today the stock market went crazy once again. "Leading Indicators" is made up of such secret and exciting components such as market's development last month, bond market developments, and a lot of other actually publically available variables. Guess who "positively surprised". Well, the stock and bond markets. How can the realized stock market performance surprise? At least that is what the media wanted you to believe. Smarter money sold the figure.

A more interesting number is consumer sentiment, charted below together with private consumption. "Look down below!"

A more interesting number is consumer sentiment, charted below together with private consumption. "Look down below!"

25 April, 2008

What is the value added by an equity analyst?

The chart below seems to indicate that analysts' forecasts merely are a moving average of actually reported earnings. Thus no predictive value whatsoever. Note how the analysts at turning points in the cycle, stubbornly continues to believe that (especially) the rise will continue.

Subscribe to:

Posts (Atom)